A tax abatement is an agreement between a local government and a property owner to exempt part of the taxes owed in return for improvements to the property. Abatements are governed by Tax Code, Chapter 312. Local taxing units can use abatements to attract development to their jurisdictions.

Why do local governments grant tax abatements?

Tax abatements reduce the cost of new development to property owners. This can help new businesses move to the region or help existing businesses expand. In return, the local government gets increased property values that will raise the tax base and, possibly, provide new jobs.

What are the benefits of a tax abatement?

While tax abatements are short-lived, they can have a significant future impact:

They reduce unemployment. A new business creates jobs. People employed by the business may use their income to build homes and buy goods and services, cars and other personal necessities.

They strengthen other businesses. Established businesses benefit when a new business opens. The increase in patrons allows other businesses to grow by investing in capital improvements and hiring new employees.

They increase tax revenue. When an abatement is offered, a city still benefits from increased tax revenues. Employees of a new business spend their money at local stores (which boosts sales tax receipts) and often build new homes (which increases property tax receipts). These things occur without the need to increase tax rates.

Tax receipts continue to grow long term after the abatement expires. Once a business is well-established within a community, the improvements and facilities that are added can be taxed. The tax rate and revenue from developed property is higher than on undeveloped property. This creates a long-term source of revenue for the city.

They provide a flexible economic development tool. Abatements can be viewed as a flexible option compared to other economic development tools since infrastructure improvements or risky building ventures could become fixed costs. Without the abatement, it may be financially unfeasible for retailers to build on a certain area, due to features like underground pipelines, stormwater storage or floodplain.

Which local governments can grant tax abatements?

Any local government that collects ad valorem tax can grant an abatement, but typically only a city or county can grant the first abatement on a particular property.

Are there any prerequisites for granting abatements?

Yes. Each taxing unit must pass a resolution stating its intention to grant abatements and establish guidelines and criteria that will govern the abatement agreements. Abatements can only be granted for property within a reinvestment zone.

Are there reporting requirements for tax abatements?

Yes. Any appraisal district that includes a tax abatement reinvestment zone or abated property must submit reports about the zone, the abatement agreements, modified or cancelled abatement agreements, if applicable, and the post-abatement reports to the Texas Comptroller of Public Accounts.

How long are the guidelines and criteria effective?

Guidelines are effective for two years from the date adopted. After they expire, the taxing unit must readopt them or create new guidelines and criteria if the taxing unit plans to continue to grant abatements. Local taxing units are encouraged to renew the guidelines and criteria before they lapse or expire; otherwise, they must start over to create the reinvestment zone.

Can the guidelines and criteria be amended or repealed?

Yes, but while they are in effect, they can only be amended or repealed with a three-fourths vote by the taxing unit's governing body. After they have expired, the taxing unit can adopt different guidelines and criteria.

Since ISDs can create a reinvestment zone but cannot give an abatement, are they required to submit the guidelines and criteria plus and the resolution to the Comptroller?

The chief appraiser is required to report guidelines and criteria to govern tax abatement agreements. School districts may not enter into tax abatement agreements after Sept 1, 2001. Guidelines and criteria or abatement resolutions are only reported for agreements executed before Sept 1, 2001.

Is an abatement void if a government’s tax abatement guidelines and criteria are not renewed after two years?

312.002(c) suggests that the guidelines last only two years unless new ones are approved. If an abatement is given during the validly existing guidelines, then the abatement is valid regardless. This is confirmed in 312.203 when discussing the expiration of reinvestment zones. The last sentence provides, “The expiration of the designation does not affect an existing tax abatement agreement made under this subchapter.”

Reinvestment Zone

Who can designate a tax abatement reinvestment zone?

The governing body of a city or a county can designate an area as a reinvestment zone.

How do cities and counties designate reinvestment zones?

After holding a public hearing and finding the area meets statutory requirements, a city or county designates a reinvestment zone by ordinance or order.

Where can cities and counties designate reinvestment zones?

A city can designate a reinvestment zone within the city limits, in the city's extraterritorial jurisdiction or both. A county can designate a reinvestment zone within the county, but only outside city limits.

Can the boundaries of two or more reinvestment zones overlap?

A reinvestment zone created by a city cannot overlap with a zone created by a county or vice-versa. Section 312.201(c) suggests that overlapping is possible in certain situations, such as between commercial and residential zones. Additionally, an existing enterprise zone created under another law constitutes a designation for a reinvestment zone and could overlap with a designated reinvestment zone created by a municipality or a county. In the event of an overlap in Section 312.201(c), the zone where the property is located is determined by the comprehensive zoning ordinance of the municipality, if available.

Does a city or county have to designate its whole jurisdiction as a reinvestment zone?

No. A reinvestment zone can be as large as the city or county or as small as one property. Cities and counties can designate multiple reinvestment zones in different sections of their jurisdictions.

What are the criteria an area must meet to be designated a reinvestment zone?

A city or county must find that designating an area as a reinvestment zone would:

contribute to the retention or expansion of primary employment; or

attract major investment in the zone that would benefit the property included in the zone and would contribute to the economic development of the city or county.

Cities must also find that the improvements sought are feasible and practical and would benefit the land included in the zone and the municipality after a tax agreement expires.

Is a Neighborhood Empowerment Zone (NEZ) (Local Government, Chapter 378) the same thing as a reinvestment zone (Tax Code, Chapter 312)? Do NEZs have a reporting requirement?

The Chapter 312 reporting requirements do not apply to a NEZ agreement.

A Chapter 378 agreement can abate municipal taxes on property in the Neighborhood Empowerment Zone (“NEZ”). It is different from a Chapter 312 agreement. Chapter 378 NEZ agreements and agreements under Chapter 312 share a couple of similarities, which are: NEZ agreements have the same 10-year duration limit as Chapter 312 agreements and when the municipality adopts a NEZ, the resolution must include a finding that the requirements under Section 312.202 as applied to the NEZ are satisfied.

Public Meetings/Public Notices

At what stage is an applicant’s name disclosed to the public by a lead taxing unit in the Chapter 312 abatement process?

A lead taxing unit includes the name of a Chapter 312 abatement applicant in the hearing notice issued for the agreement’s approval. Other information provided with an abatement application —such as specific processes, business activities, equipment or other property to be located on the land— remains confidential and is not subject to public disclosure until the abatement agreement is executed pursuant to Tax Code § 312.003. Once executed, the information is no longer confidential and is subject to public disclosure.

When must a city or county give notice of its intent to adopt an abatement agreement?

Once a reinvestment zone is designated, the governing body of a city or county may enter into a tax abatement agreement with the property owners for a period not to exceed 10 years. Once the agreement is approved by the governing body at a regularly scheduled meeting, it may be executed after notice to other taxing units.

At least 30 days’ public notice of the meeting for the approval of a tax abatement agreement is required. The notice should be given in the manner prescribed by the Open Meetings Act.

Among other requirements, the notice must contain the following:

the property owner's name and the applicant's name in the agreement;

the name and location of the reinvestment zone subject to the agreement;

a general description of the nature of the improvements or repairs in the agreement; and

the estimated cost of the improvements or repairs.

Must a city or county hold a public hearing when it grants an abatement?

The governing body must convene at a regularly scheduled public meeting to vote on approving a tax abatement agreement. By majority vote, the governing body may approve a tax abatement agreement if the terms and property meet the guidelines and criteria.

What notice is required for a public hearing about a reinvestment zone?

Once guidelines and criteria have been adopted, the governing body of a city or county may designate an area as a reinvestment zone after a public hearing.

A seven-day newspaper notice of the public hearing is required, in addition to a seven-day written notice to other taxing units in the proposed area before a public hearing may be conducted. The newspaper must be in general circulation in the city or county. Notice to the other taxing units is presumed delivered when properly addressed to the appropriate presiding officer for each taxing unit and placed in the mail or sent via registered or certified mail with a return receipt received.

The governing body of a city or county conducts the public hearing to determine whether the area for designation qualifies as a reinvestment zone. At the hearing, interested persons are entitled to speak and present evidence for or against the designation of the reinvestment zone.

Must a local taxing unit publish a public notice and hold a public meeting to adopt guidelines and criteria?

Before the designation of a reinvestment zone, a city or county must first establish guidelines and criteria governing tax abatement agreements, which must be available for both new and existing facilities/structures. The governing body of a taxing unit must hold a public hearing regarding the proposed guidelines at which the public is given the opportunity to be heard. The guidelines and criteria are effective two years from adoption and can be changed with a three-fourths vote of the governing body. A taxing unit with a website must post the adopted guidelines and criteria online.

If a public notice and copy of the proposed agreement are provided to taxing entities seven days prior to a public hearing, can the county continue to negotiate terms of the agreement during those days?

No. If the proposed agreement is changed during the seven days before the meeting, there won’t be sufficient time to provide copies of that agreement to the taxing units. According to statute, municipalities/counties must send taxing units where the property is located a notice of their intention to enter into an agreement and a copy of the proposed agreement that will be considered for approval at the meeting in accordance with Section 312.2041(a).

Should all applications be included on the County Commissioners Court agenda?

No, they are not required. The governing body of a taxing unit may delegate the authority to its employees to determine whether a particular tax abatement request or application should be considered. See Section 312.002(d)(2). However, the governing body must follow the proper procedures for delegating authority.

While written to address municipalities, does the “Notice of Tax Abatement Agreements to Other Taxing Units” (Section 312.2041) extend to counties as well?

Yes. It is covered in Subchapter C. Tax Abatement in County Reinvestment Zone, Section 312.402(a-2), which provides that “[t}he execution, duration, and other terms of an agreement entered into under this section are governed by the provisions of Sections 312.204, 312.205, and 312.211 applicable to a municipality. Section 312.2041 applies to an agreement entered into under this section in the same manner as that section applies to an agreement entered into under Section 312.204 or 312.211.”

Abatement Agreement

Can a city enter into a tax abatement with a business in its extraterritorial jurisdiction?

According to Tax Code Section 312.204(c) and Section 312.206(c), a city may enter into tax abatement agreements in its extraterritorial jurisdiction, provided all applicable conditions and guidelines are satisfied.

Should a taxing unit entering into a Chapter 312 agreement include non-boycott of Israel provisions or verification against discrimination of firearm or ammunition industries or verification against discrimination developer does not boycott energy companies

Yes, the prohibition against contracting with entities that discriminate against firearm entities or boycott energy companies or Israel applies to all state agencies and political subdivisions entering into a contract with companies for goods or services amounting to at least $100,000. For details, see this linked PDF file.

If a 10-year abatement is executed on July 1, 2024, to take effect Jan. 1, 2025, but the project experiences supply chain issues or construction delays, can the abatement term be adjusted after it has already started?

This depends on whether the agreement took effect or is in the period between the execution date and effective date.

An abatement can be modified for many reasons, including a change in effective and expiration dates, to ensure a business can receive the full 10 years of abatement. Because the lead taxing unit is one of two parties to this abatement agreement contract, it is incumbent upon the lead taxing unit to ensure no delays will affect the start of the abatement period as implemented by the County Appraisal District (CAD).

If supply chain issues or construction delays occur during the time between the execution date and the effective date, the lead taxing unit should consider changing the effective and/or expiration terms before the abatement clock begins. Note: The “in-between period” is the time frame between the “execution date” of when the abatement agreement was signed and/or approved and the “effective date” of when the abatement agreement takes effect.

Lead taxing units required to submit abatement documentation to the Comptroller’s office have two options:

Vote to approve and execute the agreement after checking if the business anticipates any delays.

Submit all required documents to the Comptroller within 30 to 60 days after the vote, or …

If there is uncertainty because of supply chain or construction delays, submit required documents to the Comptroller following the statutory allowable time. The lead taxing units engaging in abatements have until July 1 of the year following the execution date year to file with the Comptroller. This gives some leeway to work things out if there are delays, or …

Draft the agreement so the lead taxing unit and business seeking the abatement agree in principle to the terms but do not vote to approve or sign the agreement until the delays are resolved. This should be communicated between the business and the lead taxing unit.

The lead taxing unit should maintain regular contact with the business to determine if it will begin operation without delays. If delays are expected and the business will not open on time, communicate the situation to the lead taxing unit, which should inform the CAD, so the CAD doesn’t give the abatement yet to the business.

Furthermore, let’s consider three scenarios for clarity:

What if the abatement is in effect for five years but before it expires, the city wishes to extend the abatement one more year?

In this case, the abatement could still be modified, as long as the total term does not exceed 10 years.

What if a business receives an abatement contract for 10 years, but one year into the abatement term wants to modify the effective dates so the business can continue getting a 10-year abatement as it experiences delays?

In this case, the business cannot modify the abatement to change the start and end dates because the abatement term has already started, regardless of whether the CAD has started the process or abated that business’s property taxes the first year.

What if the abatement is for 10 years but it hasn’t yet taken effect?

The lead taxing unit can modify the abatement term because the business hasn’t yet received anything, and the agreement has not gone into effect. For example:

An abatement agreement between the lead taxing unit and a business is signed on June 20, 2019.

The abatement agreement as agreed to by both parties states the “effective” date is Jan. 1, 2020.

The expiration date is when the agreement concludes. In this scenario, the 10-year agreement will conclude Dec. 31, 2029.

The time between June 21 and Dec. 31, 2019, is the in-between period. The lead taxing unit should maintain contact with the business during those months to ensure work is on schedule. If the business experiences delays due to supply chain or construction issues, the optimal solution is to modify the agreement, and if necessary, submit a Modified Abatement Agreement e-form to the Comptroller as submitted by the CAD by Dec. 31, 2019.

Review Texas Attorney General opinions GA-0134 and JC-0133.

These support the statute in the following manner:

A tax abatement agreement made pursuant to Chapter 312 of the Tax Code, the Property Redevelopment and Tax Abatement Act, may not exceed 10 years. A governmental entity may not grant a tax abatement for property that previously received a 10-year tax abatement. To receive more than 10 years of tax abatement, the abatement agreement must have been made prior to Sept. 1, 1989. Tex. Attorney General Opinion JC-0133 (1999).

What are the steps for approving an abatement agreement in a city or county?

residential or commercial/industrial real property that is subject to ad valorem taxation in a reinvestment zone if the owner or leaseholder agrees to make improvements to the property;

a property owner's real property or tangible personal property that is located on the real property; and.

property subject to ad valorem taxation, including a leasehold interest, improvements or tangible personal property located on the real property that belongs to the owner of a leasehold interest in tax-exempt real property

No. Abatements cannot be granted on property owned or leased by a member of the city council, the zoning board, or the city's planning board or a member of the county commissioners court.

Each year of an abatement agreement, a local government can abate up to 100 percent of the property value minus the value of the property the year the agreement was executed.

If a lead taxing unit grants a business a 75% abatement (or any other desired percentage), are participating taxing units required to provide the same percentage?

Yes, according to Section 312.204(b). Multiple municipal tax abatement agreements with property owners within a reinvestment zone must exempt the same proportion of taxable value and must be for the same duration.

How many years can a property be abated?

A property can be abated up to 10 years per agreement.

What is the process for granting and approving an abatement?

A local government must send written notice to the presiding officer of the governing body of every other taxing unit that taxes the property. The notice must include a copy of the proposed abatement agreement and be sent at least seven days before the agreement is executed.

To be effective, a tax abatement agreement must be written and it must be approved by majority vote of the members of the governing body of the taxing unit at a regular meeting.

The abatement typically begins on Jan. 1 of the year after it is executed unless the agreement stipulates a later start date.

If two or more taxing units participate jointly in an abatement agreement and the lead taxing unit terminates their agreement with a business, does this impact other “participating taxing units’ that have an agreement with the business located in the lead taxing unit’s reinvestment zone?

If the participating taxing unit has a separate agreement with the property owner that is independent of the lead taxing unit’s agreement (i.e. the lead taxing unit is not a party to the agreement), then the termination of the lead taxing unit’s abatement agreement doesn’t impact the participating taxing unit’s agreement unless explicitly stated in the agreement. However, if a participating taxing unit opts to be bound by the terms of the lead taxing unit’s agreement pursuant to Section 312.206(a), then the termination of the lead taxing unit’s abatement agreement may affect the participating taxing unit’s abatement. See Section 312.206(a).

Which entities can grant abatements?

Any taxing unit, except a school district, that has jurisdiction over a property can grant an abatement. If the property is:

in the city limits, the city must grant an abatement before another taxing unit is allowed;

outside the city limits and the city's ETJ, the county must grant an abatement before any other taxing unit can; or

within the city's ETJ, any taxing unit can grant an abatement first.

If the county commissioners court sets the tax rate for another taxing unit, the court can offer an abatement on behalf of that taxing unit for a property the county has already abated.

An abatement agreement cannot exempt tangible personal property existing on the land at any time before the period covered by the abatement agreement (Section 312.204(a)). Although inventory and supplies usually cannot be abated, a special provision under Section 312.204(e) allows abatement agreements with respect to inventory and supplies of certain certificated carriers.

Do other taxing units have to offer the same terms as a city or county?

No. Once a city or county grants an abatement, another taxing unit can offer an abatement to the property owner with the same or different terms.

Yes. Any time before the abatement expires, the local government can modify the terms of the agreement, assign it to a new owner of the property or cancel the agreement entirely.

Yes. If the property owner fails to make the agreed upon improvements, the taxing unit can recapture tax lost because of the abatement. If the agreement includes the required provision, a taxing unit can also recapture taxes if the property owner fails to create an agreed upon number of new jobs or fails to meet any other provision of the agreement.

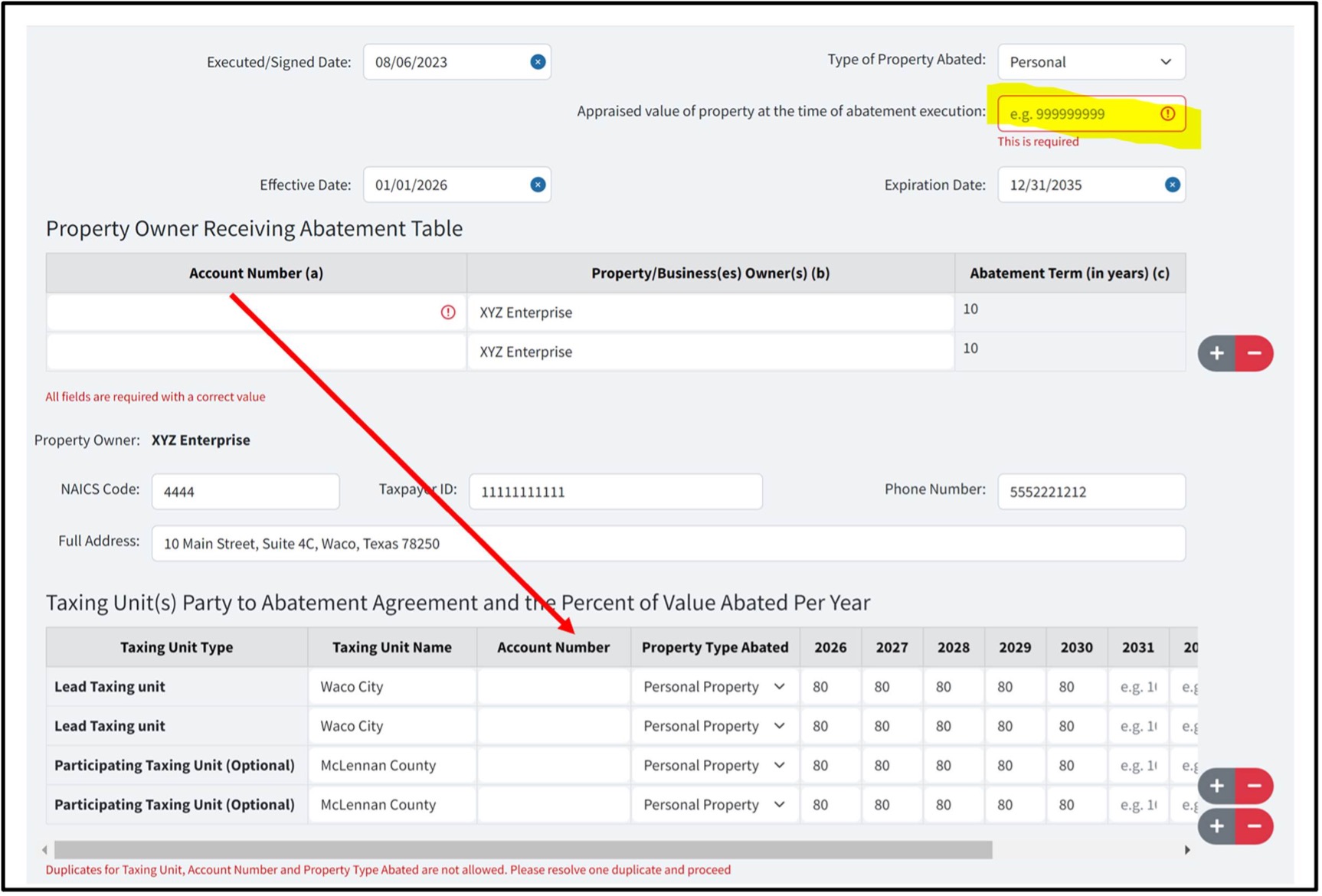

How do CADs report the value of future property in the eSystems online New Abatement Agreement form?

When an agreement between the taxing unit and a business is executed pertaining to the abatement of a property that will be built in a future year (2+ years), the CADs are unable to report the value of the “abated tangible personal property” (see yellow highlighted section below) because the property is yet to be built.

Because no such personal property exists, this means the CAD cannot yet assign an account number for the tangible personal property (red arrow seen below).

Sample Scenario

XYZ enterprise has been granted a 10-year abatement for construction of wind turbines. These turbines will be constructed on 25 acres that belong to landowner Joe Smith. Joe has agreed to lease his land to XYZ for placement of wind turbines. There is no abatement given to Joe. Primary use of the land will remain agricultural. The appraisal district’s account number for the land is 1-00000-0241-03-01800. Legal description of the land is: Abstract 241, Section 3, Tract 18.

Two Solutions:

Note: The response provided in the New Abatement Agreement online form will need to be updated on the Modified Abatement Agreement online form.

Solution 1 – Recommended Response

For future construction of personal property improvements without assigned account numbers at the time of reporting, provide the account number associated with the location of the future improvements on the online New Abatement Agreement form. This property is not included in the abatement but provides the location of the future improvements. You also can report the appraised value of the abated property at the time of the abatement execution as $0.

Account Number: 1-00000-0241-03-001800 Parent; or R123478

Parent Appraised Value of Abated Property at Time of Abatement Execution: $0

Include the location’s account number with the word “Parent” at the end. When the property is added to your appraisal roll, update the account number field in the online Modified Abatement form with the account number associated with the abatement.

Solution 2 – Alternate Response

Because there is no personal property yet on the land at the time of the agreement’s execution and won’t be for more than a year, a possible response would be for the CAD to report zeroes in the account number fields and in the appraised value of the abated property at the time of abatement agreement on the online New Abatement Agreement form.

Account Number: 00000

Appraised Value of Abated Property at Time of Abatement Execution: $0

When the property is added to your appraisal roll, update the account number field in the online Modified Abatement form with the account number associated with the abatement.

Who is required to submit reports to the Comptroller?

The chief appraiser of each appraisal district containing a reinvestment zone or executing a tax abatement must report information about the zone and the abatement to the Comptroller. However, the taxing units must provide the relevant information.

What does the Comptroller do with the information submitted?

The Comptroller compiles information about reinvestment zones and abatements and submits a report to the Legislature and the governor before each legislative session. Information about all reinvestment zones and abatements are publicly available in the searchable databases found here on Comptroller.Texas.Gov.

The Comptroller's Data Analysis and Transparency Division can answer questions by phone at 800-531-5441 ext. 5-0664 or by email. Additional information can be obtained by submitting a written request to open.records@cpa.texas.gov.

Post Abatement Property Value Reports

Who must report post abatement property values?

Chief appraisers of appraisal districts with tax abatement agreements.

What is the purpose of post abatement property value reporting?

The purpose of the reports is to ensure the abatement permanently increased property values rather than giving a temporary boost or resulting in a business that is willing to leave the community.

How is the report filed?

The Post Abatement Property Value Report is filed using eSystems. For more information, refer to Submitting Required Reports.

Should the report be filed for cancelled or terminated tax abatement agreements?

No.

What is the deadline for filing the Post-Abatement Valuation Report, and how often must it be submitted?

The first annual report is due one year after the expiration of the tax abatement agreement and the second and third reports the following years.

If two or more taxing units participate in an abatement agreement with a business, and the lead taxing unit terminates its agreement, does this affect the other participating taxing units that have an agreement with the business in the lead taxing unit’s reinvestment zone?

If the participating taxing unit has a separate agreement with the property owner that is independent of the lead taxing unit’s agreement, then termination of the lead taxing unit’s abatement agreement would not impact the other taxing unit’s agreement — unless explicitly stated in the original contract. However, if a participating taxing unit opts to be bound by the terms of the lead taxing unit’s agreement pursuant to Section 312.206(a), then termination of the lead taxing unit’s abatement agreement may affect the participating taxing unit’s abatement. See Section 312.206(a).

What happens if the current year's appraised value of a property is not available?

Report the preceding year's appraised value if the current year's appraised value is not available at the time the Post Abatement Valuation Report is filed.

How does a chief appraiser report the appraised value of multiple properties that were subject to a tax abatement agreement?

The Post Abatement Valuation Report allows multiple properties associated with a tax abatement agreement to be included in one submission. To add another property to the form, select “Yes” to the last question, which asks whether there are additional properties/lots associated with the agreement, and then input your answers to the questions for that property. Continue to answer “Yes” to the last question until you have added all properties associated with the agreement.